Assessing Deere’s (DE) Valuation After US$20b US Manufacturing Expansion Plan

Expansion in Indiana and North Carolina puts Deere (DE) in focus

Deere (DE) is drawing fresh attention after outlining a $20b plan to expand U.S. manufacturing. The initiative includes a new parts distribution center in Hebron, Indiana, and an excavator factory in Kernersville, North Carolina.

See our latest analysis for Deere.

The expansion plan lands at a time when momentum in Deere’s shares has been picking up, with a 1 month share price return of 21.7% and a year to date share price return of 21.5%. Over longer periods, total shareholder returns of 23.0% over one year and 93.1% over five years indicate that recent gains build on an already strong track record, as investors digest both the new U.S. manufacturing investment and recent boardroom and governance developments ahead of the upcoming earnings call.

If you are weighing Deere’s latest moves against what else is happening in industrials, it could be worth scanning aerospace and defense stocks for other capital goods names that are drawing attention.

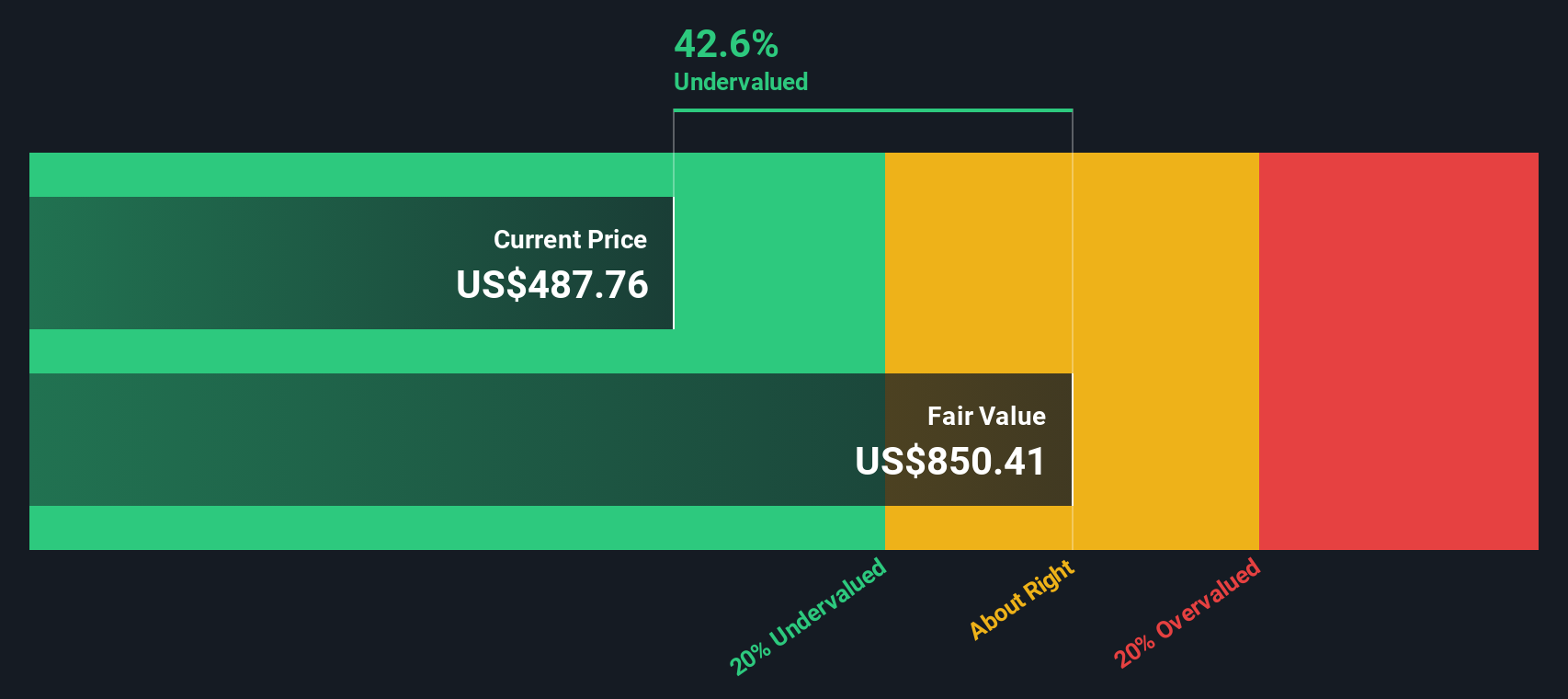

With Deere shares up around 22% over the past month and trading near US$567, the stock sits close to some analyst targets yet shows an estimated 12% intrinsic discount. This raises the question: is there still upside here, or is future growth already priced in?

Most Popular Narrative: 7.7% Overvalued

At $567.26, Deere sits above a widely followed fair value estimate of about $526.91, which is built around precision agriculture, margins, and a maturing cycle.

Rapid adoption of Deere’s precision agriculture and automation solutions (e.g., JDLink Boost, Precision Essentials bundles, See & Spray tech, and new automation features) is driving higher-value product sales and increased software engagement globally, positioning Deere to benefit from shifts toward high-efficiency, technology-enabled farming. This is expected to support both future revenue and net margins through higher-margin recurring software and data services.

Curious what kind of earnings power this assumes? The narrative leans heavily on margin expansion, recurring software revenue and a richer profit multiple. The exact numbers might surprise you.

Result: Fair Value of $526.91 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, there are clear pressure points, including higher tariff and input costs, as well as a softer North American large ag market, that could cap margins and challenge the upbeat Precision Ag story.

Find out about the key risks to this Deere narrative.

Another View: Cash Flows Point To Undervaluation

The narrative fair value of about $526.91 suggests Deere is 7.7% overvalued at $567.26, but our DCF model points in the opposite direction. On that view, the shares trade around 12% below an estimated future cash flow value of $644.77. Which picture do you think better reflects the risks and rewards?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Deere for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 867 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Build Your Own Deere Narrative

If you look at this and think the story should read differently, you can test the assumptions yourself in minutes with Do it your way.

A great starting point for your Deere research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Deere has sharpened your interest, do not stop here. Use the Simply Wall St screener to spot other stocks that might fit your style and goals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com