(Photo: Adobe Stock / Chopang Studio)

(Photo: Adobe Stock / Chopang Studio)

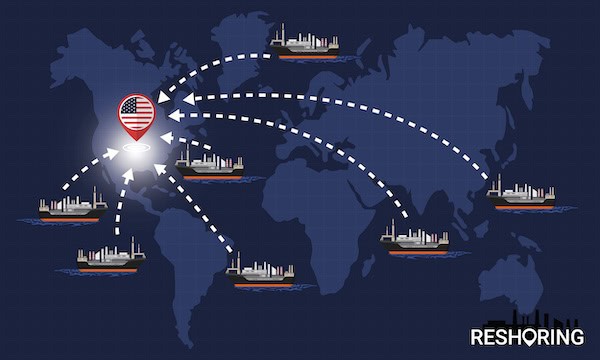

The trend among so many American companies of reshoring—bringing manufacturing and more back to the United States—is proving to be seismic. Under President Donald Trump, many major companies have announced large investments in U.S. production expansions during 2025 and now in 2026, signaling a shift back toward domestic production in strategic sectors.

GlobalFoundries, for one, has said it is investing $16 billion to reshore chip manufacturing. Stellantis, the owner of Jeep, Ram, Dodge, unveiled a $13 billion U.S. manufacturing investment. And Johnson & Johnson plans to spend $55 billion to build facilities in the United States, partly responding to trade and supply chain pressures.

Federal announcements in 2025 point to more than $200 billion in multi-year U.S. investment commitments, led by major life sciences companies. In addition to Johnson & Johnson, other significant announcements came from AstraZeneca ($50 billion), Bristol Myers Squibb ($40 billion), GSK ($30 billion), and Eli Lilly and Company ($27 billion). While not always labeled as reshoring, these projects represent significant domestic capacity expansion aligned with federal priorities.

Activity has been especially concentrated in four sectors: pharmaceuticals, semiconductors, advanced manufacturing, and energy and data infrastructure—industries increasingly tied to national security and supply chain resilience.

On the employment side, reshoring and foreign direct investment continued to generate substantial, if moderating, gains. Approximately 244,000 U.S. jobs were announced in 2024, down slightly from the 2023 peak. While investment momentum remained strong in 2025, job creation is scaling more gradually as projects move from announcement to operation.

These investment announcements are significant, and jobs numbers are substantial compared with historical levels. Companies have cited numerous reasons for bringing manufacturing or business operations back home after they had previously been moved overseas. These include supply chain reliability, tariffs or trade policy changes, rising overseas labor costs, automation reducing labor-cost advantages, national security concerns, and Made in USA branding benefits.

American Machinist is reporting that industry surveys and analyses suggest that reshoring will continue to grow if the U.S. significantly expands its skilled manufacturing workforce. In fact, if American companies can fill more skilled jobs, some studies estimate that a meaningful share of currently off-shored production—as much as 30% of OEM-offshored products—could come back.

Reshoring: A Broader View

“Reshoring to the U.S. has experienced steady, moderate growth over the past 10 years, and I expect that to continue,” predicts Rosemary Coates, Executive Director of the Reshoring Institute in Los Gatos, CA, which provides expert guidance on global manufacturing strategy.

“The bigger story is that now companies are considering the global landscape and choosing multiple places to source and manufacture,” Coates continues. “This new way of thinking mitigates the risks of regionalized disasters and geopolitics and allows companies to take advantage of low-cost labor. It is also an opportunity to develop new markets and customers and manufacture products close to where they are sold, thereby reducing carbon footprint and developing sustainability programs. What I see is not just reshoring, nearshoring, or friendshoring, but global supply chain management that is rethinking its world.”

She adds, “What we are seeing from our Reshoring Institute clients is a movement away from China and into other Asian countries and Mexico. Mexico has become a very attractive destination because of its low-cost labor and rapidly developing manufacturing capabilities.”

Still, geopolitics and the Trump Administration’s changing tariff policy has made selecting alternate global manufacturing locations a challenge. Says Coates, “Companies are unsure of what tariffs might be imposed, causing additional costs on importing raw materials, parts, and finished products. While long-term, this may result in reshoring, in the short term, it increases costs.”

Long before a site selection begins, Coates explains, the Reshoring Institute encourages companies to analyze their product cost structures so that they have a clear picture of the percentage of production that is related to materials and what percentage is related to labor. She points out: “If labor is greater than 50% of the overall cost, then a low-cost labor area is very important.”

(Image: Adobe Stock / Foxeel)

(Image: Adobe Stock / Foxeel)

Foreign-Trade Zones: Place To Land

Jeffrey J. Tafel, CAE, President of the National Association of Foreign-Trade Zones (NAFTZ), emphasizes that foreign-trade zones are “a proven competitiveness tool for reshoring, helping manufacturers/importers/exporters lower total landed costs, mitigate tariff exposure, defer duties and improve cash flow—often enough to shift the ROI in favor of U.S. investment.”

NAFTZ, an association of public and private members, is the collective voice of the U.S. Foreign-Trade Zones Program. Association members increasingly use foreign-trade zones not just for duty savings, Tafel explains, “but as resilience platforms that enable flexible sourcing, domestic assembly, and faster response to customers. For nearshoring in Mexico and Canada, U.S. FTZs complement USMCA (The United States-Mexico-Canada Agreement) by supporting more integrated North American supply chains—allowing firms to optimize cross-border flows while keeping higher-value operations anchored in the U.S.”

Cost volatility, supply chain risk, geopolitics and customer proximity are all converging to reshape sourcing strategies.

“NAFTZ consistently hears that unpredictable tariffs, shipping disruptions and geopolitical exposure have made ‘lowest-cost country’ models far riskier,” says Tafel, “while U.S. FTZ benefits and state and local incentives materially narrow the cost gap for U.S. locations. Being closer to customers improves speed and customization, making reshoring and nearshoring a strategic risk management decision, not just a cost play.”

Supply chain resilience has helped change the way manufacturers evaluate sites today compared to five years ago. Says Tafel, “Site selection has shifted from a primary focus on labor and tax incentives to a broader resilience lens that prioritizes logistics access, supplier redundancy, regulatory readiness and the ability to pivot sourcing quickly.”

From NAFTZ’s perspective, companies are integrating trade compliance and tariff strategy earlier in site selection—recognizing that operational flexibility and trade tools like U.S. FTZs are now core competitive advantages, not back-office considerations.

Many firms are positively surprised by how much total landed cost can be reduced through U.S. FTZ benefits, incentives, and logistics efficiencies when viewed holistically, Tafel points out. “Similarly, companies often underestimate the true cost of offshore complexity—inventory carrying costs, compliance burdens, disruption risk and lost revenue from slow response times—which reshoring can materially reduce.”

Case In Point: John Deere, GE Appliances

Other companies are likewise looking forward and underscoring that there is no place like home.

In keeping with its self-described “strong tradition of building America,” Moline, IL-based John Deere has rolled out plans to open two new U.S.-based facilities: a state-of-the-art distribution center near Hebron, IN, and a cutting-edge excavator factory in Kernersville, NC. Both are set to open within the next year.

The Kernersville campus reshores manufacturing and production from Japan. The company already operates over 60 facilities across more than 16 states.

“Our investment in these new facilities underscores John Deere’s dedication to strengthening the backbone of American industry and supporting local economies,” said John May, Chairman and Chief Executive Officer of the manufacturer of agricultural, construction, and forestry machinery, turf care equipment and diesel engines. “We believe in building America, and these projects represent our intent to continue driving innovation and job creation in the United States.”

“These investments further demonstrate our commitment to invest $20 billion in U.S. manufacturing over the next 10 years,” May said.

Another example: last summer, GE Appliances, a Haier company, said it would invest more than $3 billion over the next five years in its U.S. operations, workforce, and communities. The first phase of investments will begin at GE Appliances plants in Kentucky, Alabama, Georgia, Tennessee, and South Carolina. Upon completion of this plan, GE Appliances will have invested $6.5 billion across its U.S. manufacturing plants and nationwide distribution network since 2016.

Workforce “Foundational”

What lies ahead? Workforce availability and skills are “foundational” to reshoring decisions, NAFTZ’s Tafel believes, even as expectations evolve toward technical roles supported by automation.

And Coates observes, “While workers may be available, they often do not have the skills to operate in a sophisticated and automated manufacturing environment. I often say we have a skills shortage in the U.S., not a labor shortage. There needs to be more emphasis on education—particularly engineering—and the development of community college programs and apprenticeships.”

With more than 4,000 new U.S. jobs added since 2016, and more than 1,000 new jobs anticipated from its five-year plan, GE Appliances places employees as central to its growth strategy.

“Infrastructure and tools matter, but they are not enough,” said Bill Good, GE Appliances’ Vice President of Supply Chain. “America’s manufacturing renaissance will be built by people. That’s why we’re partnering with universities, technical schools, and high schools to develop the next generation of manufacturing leaders. We’re not just bringing jobs back—we’re bringing purpose, pride, and possibility back to American industry.”

For its part, NAFTZ sees firms pairing FTZ-enabled cost savings with deeper investments in training partnerships and workforce pipelines to make reshoring viable, increasingly prioritizing regions that can demonstrate sustained talent development and adaptability.

Tafel maintains that reshoring’s momentum will depend on policy stability, predictable trade and tariff regimes, workforce readiness, and sustained infrastructure investment.

“NAFTZ believes momentum will continue if companies can plan with confidence—knowing U.S. FTZs, incentives, and trade programs will remain reliable tools to offset cost pressures,” he concludes. “Increased policy volatility or talent constraints would risk slowing the pace of investment.”

— Snapshots —

Snapshot: Puerto Rico

Puerto Rico offers a compelling reshoring value proposition as a U.S. jurisdiction with global reach. Companies benefit from full access to the U.S. market, strong legal and intellectual property protections, and eligibility for federal programs, while operating within a cost-competitive structure. The island’s long-standing manufacturing base, particularly in biosciences, medical devices, and advanced manufacturing, is supported by a highly skilled, bilingual workforce and mature supplier networks.

Puerto Rico’s strategic location provides efficient access to North America, Latin America, and Europe, helping companies reduce transit times and strengthen supply chain resilience. Incentives under Act 60 and a streamlined business-establishment process further enhance competitiveness for high-value operations, particularly those seeking long-term operational stability within the U.S.

Recent expansions reinforce this momentum. Amgen, Eli Lilly, CooperVision, Terumo, Millicent Pharma, and others continue to invest and expand on the island —underscoring Puerto Rico’s role as a proven reshoring destination within the United States.

Snapshot: U.S. Virgin Islands

As companies rethink global supply chains, the U.S. Virgin Islands (USVI) emerges as one of the most strategically advantaged U.S. jurisdictions for reshoring and nearshoring. As a U.S. territory outside the U.S. customs zone and exempt from the Jones Act, the USVI allows foreign-flag vessels to move goods directly between the Territory and global markets, reducing shipping constraints and expanding routing options.

On St. Croix, the South Shore Trade Zone features commercial land for development, available warehouse space, and direct access to deep-water ports accommodating drafts of up to 30 feet. An international airport in the zone, with warehouse facilities in close proximity, further enhances multimodal connectivity, enabling efficient movement of goods from port to port and air to sea.

Coupled with competitive tax incentives and a stable U.S. legal framework, the USVI stands out as a resilient, flexible, and globally connected destination for manufacturers, logistics providers, and distributors positioning for long-term growth in the Americas and beyond.

Source link

Courtesy: photo by Julia on Pexels

Courtesy: photo by Julia on Pexels