Manufacturing Construction Spending Declines Under Trump

Spending to build, expand and rehabilitate manufacturing sites in the U.S. has declined since President Donald Trump took office, according to U.S. Census Bureau data. Yet, Trump has repeatedly boasted that “factory construction” is up 41%.

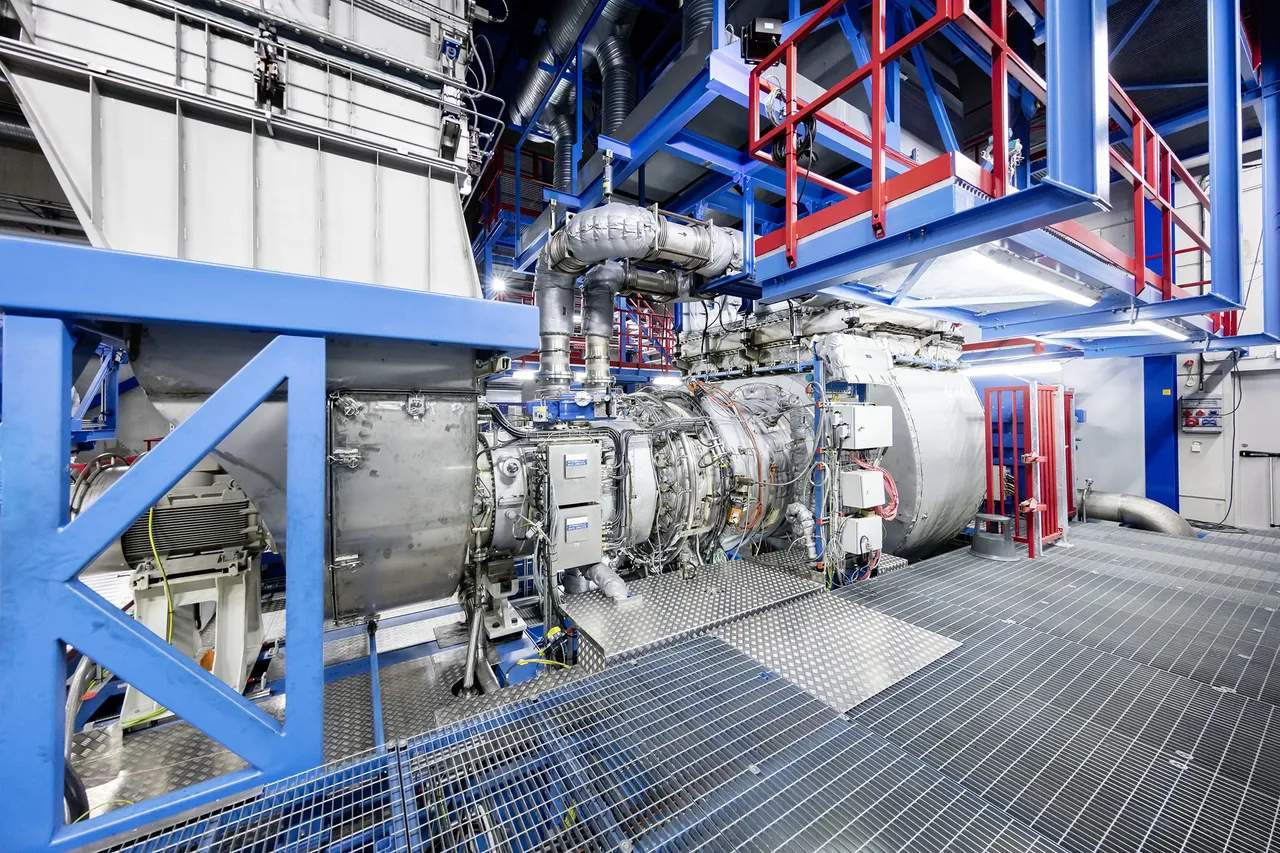

A general view of the Samsung Austin Semiconductor plant on April 16, 2024, in Taylor, Texas, which received CHIPS Act funds. Photo by Brandon Bell/Getty Images.

A general view of the Samsung Austin Semiconductor plant on April 16, 2024, in Taylor, Texas, which received CHIPS Act funds. Photo by Brandon Bell/Getty Images.

Trump cited the 41% statistic in a White House press conference on Jan. 20 – calling it a “record” increase and suggesting that other presidents cannot compare to this “record.”

“Investment in American factories is up 41%. That’s a record. Nobody goes 41% up. You go 2% up, 1% up. You go down by 3%. If Kamala [Harris] got elected, the 41% up would be 41% down,” Trump said at the press conference, referring to the former vice president and Democratic presidential nominee who lost to Trump in the 2024 election.

A day later, in a Jan. 21 speech at the World Economic Forum Annual Meeting in Davos, Switzerland, Trump repeated the 41% figure.

“Factory construction is up by 41%, and that number is really going to skyrocket right now, because that’s during a process that they’re putting in to get their approvals and we’ve given very, very quick, fast approvals,” Trump said.

This claim is part of a theme the president has emphasized of a “manufacturing boom” or “booming” economy due to his trade policies.

At our request, the White House sent us a link to the Census Bureau’s manufacturing construction spending data via the Federal Reserve Bank of St. Louis’ online database known as FRED. We provide more about the White House response later, but let’s focus first on what the data show.

Under President Joe Biden — who served from Jan. 20, 2021, to Jan. 20, 2025 — there was a significant increase in manufacturing construction spending in all four years, according to the Census Bureau’s annual average estimates. After declining 6.9% in 2020 – the last year of Trump’s first term – manufacturing construction spending started to rise in 2021, the data show.

(Technical note: The Census Bureau provides average quarterly and annual estimates and monthly reports for construction spending, including manufacturing construction spending, based on its monthly Value of Construction Put in Place survey. We use all three in this story.)

Initially, the increases during the Biden years were in response to the COVID-19 pandemic, Anirban Basu, chief economist for the Associated Builders and Contractors, an industry trade association, told us in an email.

“Supply chain disruptions at the start of the COVID-19 pandemic convinced many producers to reshore capacity, while a sudden and sharp increase in construction materials prices—which rose more than 40% during the early years of the pandemic—also boosted nominal construction spending,” Basu said.

Manufacturing construction spending accelerated after Biden signed legislation in August 2022 designed to encourage private investment in U.S. manufacturing for semiconductors and clean energy. The bipartisan CHIPS Act, for example, included $39 billion to help fund semiconductor manufacturing facilities in the U.S., as explained in an April 2023 report by the Congressional Research Service.

During Biden’s four years, the annual average rate of manufacturing construction spending jumped more than 200%, from $75.5 billion to $235.6 billion, according to Census Bureau estimates. Spending surged 62% in a single year – 2023, a year after Biden signed the CHIPS Act.

But manufacturing construction spending peaked in the third quarter of 2024 and has been trending down slightly ever since. Census Bureau quarterly data show that under Trump, measuring from the last quarter in 2024 through the third quarter in 2025, spending declined 6.7%.

That decline is expected to continue in 2026 and 2027, according to the most recent survey of construction economists that is conducted twice a year by the American Institute of Architects.

“Manufacturing construction spending has seen phenomenal growth in recent years, increasing by over 50% in 2022, another 62% in 2023, and then another 16% in 2024,” the AIA consensus construction forecast published Jan. 15 said. “However, growth paused last year as spending in this category fell about 5% and is projected to decline another 4% this year and 1% in 2027.”

Despite the slight declines, the AIA construction forecast noted that the semiconductor fabrication plants continue to fuel manufacturing construction spending and will do so in the long term.

“The longer-term prospects look much more promising, as construction starts for manufacturing projects have shot up again,” the AIA forecast said. “Since many of these starts are for megaprojects, such as large semiconductor fabrication plants that entail a complex construction process, it may take a while before the activity shows up in the construction spending data.”

In January, Basu analyzed the Census Bureau’s most recent monthly report for nonresidential construction spending, which showed manufacturing construction spending as of October had declined for nine straight months.

“With CHIPS Act-enabled megaprojects winding down and the stiff headwind of trade policy, manufacturing construction spending has fallen by nearly 10% over the past 12 months, accounting for more than the entire decline in private nonresidential spending,” Basu said in an ABC press release issued Jan. 21. (By “trade policy,” Basu is referring to the economic impact of Trump’s tariffs on construction materials.)

On a monthly basis, the Census Bureau shows a 7.3% decline in manufacturing construction spending last year under Trump from January through October, the most recent data available.

Beginning on Jan. 23, we asked the White House on multiple occasions to provide support for the 41% figure used in Trump’s Jan. 20 and 21 remarks. After not receiving a response, we sent another email on Feb. 2 after the president wrote an opinion piece for the Wall Street Journal on Jan. 30 that said, “Factory construction is up by 42% since 2022.” We asked how it arrived at a 42% increase “since 2022.” That evening, the White House sent us a link to the Census Bureau’s manufacturing construction spending data, saying it compared “averages of Jan – August 2025 vs 2021-2024 average.”

That’s true — as far as it goes. On an annualized basis, monthly manufacturing construction spending averaged $226.1 billion for January through August — which is 40% higher than the annual average of $161.1 billion in Biden’s four years. But Trump wrote that the 42% increase was “since 2022,” not 2021. (We’ve asked the White House for a clarification.)

More importantly, the White House methodology fails to take into account the 212% increase in factory construction spending over Biden’s four years, which peaked in 2024 at an annual average of $235.6 billion, and how the Biden-era CHIPS Act continues to fuel manufacturing construction spending.

As we noted earlier, Basu attributed the recent decline to Trump’s tariffs and the slowing — not the halting — of construction projects spurred by the CHIPS Act. Asked to elaborate on his analysis, Basu told us that the manufacturing construction spending in 2025 is “largely due” to the CHIPS Act.

“While spending in the segment remains elevated from 2022 levels, that’s partially due to a precipitous increase in materials prices that occurred in 2022 and 2023 — these data are in nominal terms — and largely due to the surge in megaproject activity induced by the CHIPS Act,” Basu said.

He added that Trump’s tariffs have helped drive up the costs of fabricated metal — which has increased manufacturing construction costs.

“[I]t should be noted that spending in the fabricated metal manufacturing subsegment is up 19% over the past year,” Basu said. “Some of the increase can be contributed to tariffs and the resulting increase in demand for domestic production.”

We should note that even with the recent surge in manufacturing construction spending, there has been a decline in the number of manufacturing jobs. As we reported last month, the economy lost 63,000 manufacturing jobs in Trump’s first 11 months. That followed a loss of 98,000 in the preceding 11 months, according to the Bureau of Labor Statistics.

Shortly before Biden left office, Manufacturing Today, a trade magazine, wrote in December 2024 that manufacturing jobs were slow to materialize despite Biden’s incentives to spur manufacturing construction. But the magazine predicted the jobs “will materialize in the future.”

“Unlike traditional industrial projects, today’s semiconductor and clean energy facilities require longer timelines,” the article said. “Factories of this scale can take two to three years to complete, with even longer delays for more complex facilities, such as semiconductor plants. This extended timeline means the full benefits will not be realized for several more years.”

Basu agreed that CHIPS-related spending will result in an overall increase in U.S. manufacturing jobs – but cautioned that the impact of Trump’s tariffs could offset those gains.

“The massive facilities incentivized by the CHIPS Act will employ thousands of people,” Basu told us. “That said, all else is not equal, and recent trade policy and the effects on manufacturing input prices have put downward pressure on the industry’s employment.” (Input prices are costs of materials and other resources manufacturers need to produce goods, with some of those materials being imported.)

Others are bullish that Trump’s trade policies will encourage more manufacturers to expand in the U.S.

In April, when Trump announced higher tariffs on nearly all foreign imports, Morgan Stanley analyst Chris Snyder called tariffs “a positive catalyst” for relocating manufacturing to the U.S. More recently, Snyder said in a podcast last month that the tariffs have changed the “supply chain cost calculation” and will result in new U.S. factories.

“What we’re seeing is the cost of imports have gone higher with tariffs, and now it’s more economically advisable for these companies to make the product in the United States,” Snyder said. “And if that’s the case, that means that when they need a new factory, it’s going to come to the United States. They might not need a factory now, but when they do, the U.S. is at least incrementally better positioned to get that factory.”

In a January news article, the Wall Street Journal wrote that Trump’s tariffs “haven’t worked, so far.” The article said tariffs have increased manufacturers’ costs for foreign parts, adding that the “White House’s stop-and-start” tariff policy announcements have “also led to what many executives view as a lost year for investment.”

In a December interview with the Wall Street Journal, Trump cited — as he often does — the value of investments that he says his administration has secured to date. (As we’ve written, he has exaggerated pledges to invest made by various companies and countries that may or may not materialize, experts say.) But he couldn’t say if the investments would show results in time for the midterm elections, when the Republican Party is in jeopardy of losing its slim majority in the House. “I can’t tell you. I don’t know when all of this money is going to kick in,” the president told the Journal, adding that it may happen in the second quarter of this year.

What will happen in the coming months and years remains to be seen. But what we can say is that factory construction so far has declined under Trump and his claim that it has increased 41% depends on a spending surge that occurred under Biden.

Editor’s note: FactCheck.org does not accept advertising. We rely on grants and individual donations from people like you. Please consider a donation. Credit card donations may be made through our “Donate” page. If you prefer to give by check, send to: FactCheck.org, Annenberg Public Policy Center, P.O. Box 58100, Philadelphia, PA 19102.

Buy

Buy

This gradual slowdown is, to some extent, a continuation of decades-long trends that shifted factory jobs overseas and accelerated the decline of Midwestern cities. In an industry where capital planning and construction cycles often span several years, reversing these trends will not happen overnight.

This gradual slowdown is, to some extent, a continuation of decades-long trends that shifted factory jobs overseas and accelerated the decline of Midwestern cities. In an industry where capital planning and construction cycles often span several years, reversing these trends will not happen overnight.